You may think the new ISSB standards are intended solely for the largest companies, but the interdependence between these companies and their value chain is a key element of effective ISSB disclosure, and is increasingly pulling the typical suppliers, ie SMEs into the reporting orbit of large/public companies, parking sustainability risks and opportunities very much at the SME’s front door. So we will dive in right here: ISSB – One in, All in: Spotlight on SMEs

Because sustainable reporting is currently discretionary for SMEs, they are faced with a choice: carry on BAU and Risk the potential fallout or get ahead and leverage the Opportunities of incorporating proportionate sustainability planning into strategy.

Background:

In November 2021 following COP26 the IFRS established the International Sustainability Standards Board or ISSB, in response to urgent calls from markets, regulators and NGOs around the world to develop a single, cost effective and practical process for providing corporate sustainability disclosures, and assuring against such information.

One of the key tasks was to halt and consolidate the proliferation of competing standards and frameworks that were emerging in response to the demand for sustainability data from stakeholders such as investors, banks, customers and suppliers.

By June 2023 the ISSB had effectively consolidated the ‘best of’ sustainability disclosure frameworks including SASB, CDSB and the TCFD amongst others, and distilled their thought leadership into the first two (out of potentially four) Disclosure Standards:

- IFRS S1 General Requirements – a stock-take on whether risks and opportunities linked to sustainability could have a material impact on a company’s financial performance over the medium to long-term.

- IFRS S2 Climate-Related Disclosures – requiring information on material risks and opportunities presented by climate change and its potential impact on financial performance.

Who is ISSB aimed at?

The IFRS is acting in response to demand from the Capital Markets industry to put TCFD into practise, providing comparable and ‘decision-useful’ information in a format based on recognised accounting frameworks.

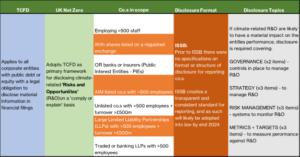

The UK Government has adopted TCFD-based reporting into law as its strategic cornerstone for delivering on its Net Zero Strategy for 2050, and pulls any company into scope that meets the following criteria:

So logically, if a company is in scope for TCFD, it will also be in scope for ISSB, currently that’s around 1,300 UK companies, and more likely to expand than shrink. Although ISSB reporting is not currently in law – it is likely to become mandatory by the end of 2024.

What about the SMEs?

There are over 5.5m SMEs in the UK responsible for over 50% of its GHG emissions. Their contribution towards reaching Net Zero by 2050 is critical, however sustainability reporting for this group is not yet mandatory. Given that 1.4m UK SMEs are employers (vs non-employers), and according to the FSB around 77% of UK SMEs are part of a supply chain, a simple estimate suggests around 1m UK ‘employing’ SMEs sell into supply chains.

Why should an SME disclose voluntarily?

- Strategy. Going back to the ISSB S1 General Requirements for large companies, it is clearly explained in the Strategy Topic that materiality includes exposure to sustainability-related R&O in its value chain, including:

“…resources and relationships in the entity’s operations, such as human resources; those along its supply, marketing and distribution channels, such as materials and service sourcing, and product and service sale and delivery…”

A supply chain impact assessment is required even when there is a significant event that does not involve the buyer – the burden of disclosure is on the reporting entity.

BUT – the buyer will not disclose unilaterally: in order to meet these external risk disclosures it will require detailed information from its vendors – ie the SME in the majority of cases. Such provision of relevant information up the chain is becoming business critical for suppliers and presents its own set of risks and opportunities.

- Scope 3:

In addition, ISSB specifies that companies will need to disclose Scope 3 emissions using GHG Protocol – that is the emissions produced from its value chain. Scope 3 is a controversial indicator and prone to very subjective input, but that input will be fed up to the company primarily by its external suppliers.

How does an SME report on climate risk?

The IFRS is in the process of adapting its “IFRS for SME Accounting Standard” to include proportionate climate related disclosures for SMEs in relation to sector, size, resources and relevant expertise, and currently request SMEs to consider the impact of climate change when applying the current standard – if they are material then it is strongly encouraged to disclose them.

What should an SME consider reporting?

Climate-related impacts are material if they affect an SMEs operations and ability to do business. These could include for example:

Example Climate Related Disclosures using IFRS for SME Accounting Standards

When should an SME start thinking about sustainability planning?

ISSB S1 and S2 came into effect on January 1st 2024, for financial reports being published in 2025. As mentioned ISSB remains voluntary, however most in scope companies will be happy to incorporate ISSB for the sake of convenience, comparability and simplicity. They will also be under pressure from stakeholders to accelerate incorporation. This suggests ISSB will move quite rapidly and probably precede any decisions on mandatory adoption. In which case SMEs will start to feel the pressure sooner rather than later.

For more information on how to build and manage your sustainability strategy to benefit your business and serve your corporate supply chains, contact The Disruption House or email info@thedisruptionhouse.com

Additional references:

https://www.british-business-bank.co.uk/research/smaller-businesses-and-the-transition-to-net-zero/